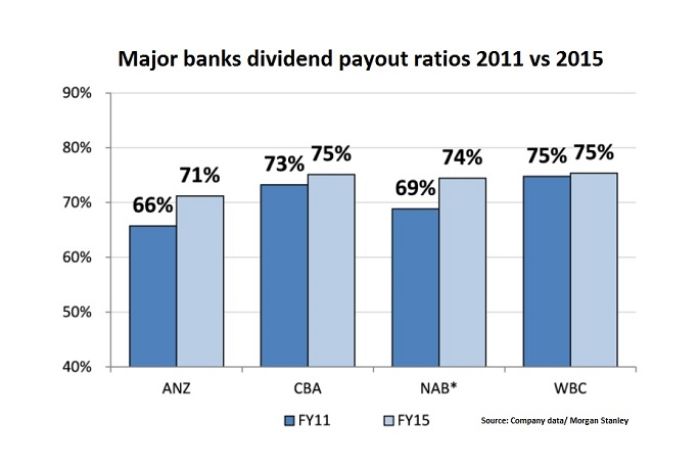

Bank pay-out ratios are high, really high. This is the dividend paid to shareholders from profits with ANZ sitting at 71%, NAB is 74%, CBA is 75% and WBC is also 75% of profits paid to shareholders. Then the argument reverts to greedy shareholders taking all the money that should be the people's money. Hang on, the federal government once attempted to nationalise the banks directly after world war and spent the next twenty five years out of government, so this isn't the answer.

Banks are commercial entities and make profits; they are also the nation's largest corporate taxpayers with CBA paying $3.3 billion in tax. This was followed by WBC with $3 billion, NAB with $2.4 billion and ANZ paid $2 billion paid in tax. Approximately 168,000 people are employed in the banking sector in Australia with the finance and insurance sector the 11th largest employer in the country.

So who are the shareholders? To begin with, anybody who has held employment over the past 25 years or so will be holding money in a superannuation account of some form. The default plan for a superannuation fund is a balanced plan generally holding approximately 25% of their assets in Australian equities. The superannuation funds of Australia are the majority owners of Australian banks with the members of the funds collectively owning the assets of the fund.

The big four banks lead the top four positions in the Standard & Poor's ASX 200 index in terms of market capitalisation with CBA making up 9.25% of the index, WBC the second largest bank accounts for 6.9% of the index, ANZ makes up 5.5% and the smallest of the the big four banks is NAB with 5.25% comprising of approximately 27% of the value of the Australian sharemarket.

So we are the shareholders and the profits are paid out to our retirement accounts. The average worker has the ability to contribute extra funds to their superannuation fund through salary sacrifice increasing their retirement benefits. But most prefer to spend it now and rely on the aged pension instead, then complain when the federal government raises the pension age as the country can't afford it.

Alternately, salary earners could directly purchase shares in banks or other investment opportunities but mostly chose not too. Instead of wagering cash on horses down the racetrack, lotto, poker machines or at the casino maybe people would be better off investing their excess funds for their future and cut down on cigarettes and alcohol to make some savings. I have done some calculations for some broke work colleagues and their nicotine habit finding they could have doubled their retirement accounts by diverting their smoking habit to investment funding.

I left school early after just turning sixteen to start an apprenticeship and I was able to take a part time evening class at my local TAFE, the Americans would know this as Community College, to learn the basics of the sharemarket. So if I am able to find the time as a guy who didn't finish high school I am sure plenty of others are capable of a little study.

This included purchasing some books and doing some extra curricula reading. If you can't afford to purchase books then the library is the answer as long as you are putting in the effort to invest in yourself. If you can't be bothered to put in the effort, then don't complain when you have to work until seventy.

No comments:

Post a Comment